|

| |

|

Polson Bourbonniere Financial

Planning Group Inc.*

DWM Securities Inc.

100 - 7050 Woodbine Ave.

Markham, Ontario L3R 4G8

Tel: 416.498.6181 or 905.413.7700

Toll Free: 1.800.263.0120

Fax: 905.305.0885 info@pbfinancial.com

www.worryfreeretirement.com

Ruth Ashton, CFP®

Investment Advisor

Certified Financial Planner

Phone: (905) 413-7710 rashton@pbfinancial.com

Paul Bourbonniere, CFP®, CLU, CH.F.C.

Investment Advisor

Certified Financial Planner

Phone: (416) 498-6181 pbourbonniere@pbfinancial.com

Lydia Bzowej, BA, CFP®, EPC Investment Advisor

Certified Financial Planner

Phone: (905) 413-7703 lbzowej@pbfinancial.com

Allan Kalin, CFP®

Investment Advisor

Certified Financial Planner

Phone: (905) 413-7706 akalin@pbfinancial.com

Derek Polson

Investment Advisor

Phone: (905) 413-7709 dpolson@pbfinancial.com

Kirk Polson, CFP®, CLU, CH.F.C.

Investment Advisor

Certified Financial Planner

Phone: (416) 498-6181 kpolson@pbfinancial.com

Office Hours

Monday to Friday,

8:30 a.m. - 5:00 p.m. |

| |

|

|

|

|

| Registered Disability Savings Plans |

| by Allan Kalin, CFP® |

Parents of children with disabilities have their own special needs when it comes to financial and estate planning. For many, the cost of looking after a disabled child would be a financial impossibility if not for the help provided by other family members such as grandparents. Parents of children with disabilities have their own special needs when it comes to financial and estate planning. For many, the cost of looking after a disabled child would be a financial impossibility if not for the help provided by other family members such as grandparents.

We now have available the Registered Disability Savings Plan (RDSP) which has been designed to provide for the long-term financial security of a person with disabilities. Contributions to an RDSP are not tax-deductible and can be made until the end of the year in which the beneficiary turns 59. However, it is the added benefit of government grants and bonds, combined with tax-deferred growth, which makes the RDSP a powerful investment tool.

| Contributing to an RDSP |

|

|

The person establishing an RDSP is referred to as the account holder; however anyone can contribute to an RDSP provided they have written permission from the account holder. An adult who qualifies for the Plan can be both the Plan beneficiary and the Plan holder.

| Building the Value of an RDSP |

|

|

There is no annual contribution limit to an RDSP. However, each RDSP has a

lifetime contribution limit of $200,000 per plan, and all contributions must cease

by the end of the year in which the beneficiary reaches age 59, no longer qualifies

for the disability tax credit, or passes away.

| Taxation issues |

|

|

Contributions to an RDSP are not tax-deductable. However, the growth on the contributions is tax-deferred while held within the Plan.

Consequently, while the funds received by the beneficiary will include both original contributions and earnings, that is the income, growth, CDSGs and CDSBs, income tax will apply only to the earnings portion and is paid on amounts withdrawn from the RDSP at the beneficiary’s tax rate. Therefore, contributions are not taxable when withdrawn from the RDSP.

| How the government helps |

|

|

Depending on the income of an adult beneficiary, or the net income of a beneficiary’s family in the case of a minor, and the amount of the annual RDSP contributions, the federal government will provide financial assistance to the RDSP.

| The Canada Disability Savings Grant (CDSG) |

|

|

The CDSG is available on an annual basis of up to $3,500 for beneficiaries or families with net incomes of less than $75,770. The grant will contribute $3 for every $1 contributed on the first $500 and $2 for every $1 contributed on the next $1,000, up to the $3,500 annual maximum.

Beneficiaries or families with net incomes in excess of $75,769 can receive a maximum annual grant of $1,000; the grant providing $1 for every $1 contributed up to $1,000. The maximum lifetime CDSG is $70,000 per plan beneficiary and the CDSG eligibility ends December 31 in the year in which the beneficiary turns age 49.

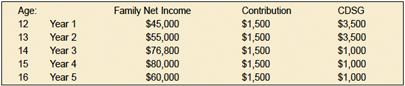

| How it works |

|

|

This chart illustrates how a family’s annual income and contribution amount determines the CDSG:

| The Canada Disability Savings Bond (CDSB) |

|

|

In addition to the CDSG, the Canada Disability Savings Bond (CDSB) is available to beneficiaries or families with a net family income lower than $37,885. RDSP contributions are not required for eligibility to the CDSB. Beneficiaries with a net income of less than $21,288 may be eligible to receive CDSB payments of $1,000 per year into an established RDSP. Where the net income is more than $21,287 but less than $37,885, a pro-rated CDSB payment of less than $1,000 will be paid into the RDSP. The maximum lifetime CDSB is $20,000 per plan beneficiary and the CDSB eligibility ends December 31 in the year in which the beneficiary turns age 49.

| How it works |

|

|

This chart illustrates how a family’s annual income and contribution amount determines the CDSB:

| Withdrawals from an RDSP |

|

|

There are two types of payments from an RDSP-Lifetime Disability Assistance Payments (LDAP) and Disability Assistance Payments (DAP). LDAPs are recurring annual payments that, once started, must be paid until either the plan is terminated or the beneficiary has died. DAPs are a lump sum payment made from the RDSP to the beneficiary or the beneficiary’s estate. Both the LDAP and DAP can be used for disability or non-disability related expenses. Only the beneficiary will be permitted to receive payments from the Plan.

| RDSP impact on other federal and provincial government programs |

|

|

RDSPs do not impact other income-tested federal government programs or the social assistance support programs of most provincial governments.

| Should you establish an RDSP? |

|

|

If you or a family member qualifies for the federal disability tax credit, there are numerous benefits to establishing a Registered Disability Savings Plan. Even if you do not have the financial means to contribute to an RDSP, you may be eligible for the Canada Disability Savings Bond, which will help you build a more secure financial future.

This article was also published in the June 2010 issue of Canadian Money Saver magazine: www.canadianmoneysaver.ca

|