|

| |

|

Polson Bourbonniere Financial

Planning Group Inc.*

DWM Securities Inc.

100 - 7050 Woodbine Ave.

Markham, Ontario L3R 4G8

Main: 416.498.6181 or 905.413.7700

Toll Free: 1.800.263.0120

Fax: 905.305.0885

E-mail: info@pbfinancial.com

Website: www.worryfreeretirement.com

Ruth Ashton, CFP®

Certified Financial Planner

Investment & Insurance Advisor

Direct: (905) 413-7710

E-mail: rashton@pbfinancial.com

Paul Bourbonniere, CFP®, CLU, CH.F.C.

Certified Financial Planner

Investment & Insurance Advisor

Direct: (416) 498-6181

E-mail: pbourbonniere@pbfinancial.com

Lydia Bzowej, BA, CFP®, EPC

Certified Financial Planner

Investment & Insurance Advisor

Direct: (905) 413-7703

E-mail: lbzowej@pbfinancial.com

Allan Kalin, CFP®

Certified Financial Planner

Investment & Insurance Advisor

Direct: (905) 413-7703

E-mail: akalin@pbfinancial.com

Derek Polson, CFP®

Certified Financial Planner

Investment & Insurance Advisor

Direct: (905) 413-7709

E-mail: dpolson@pbfinancial.com

Kirk Polson, CFP®, CLU, CH.F.C.

Certified Financial Planner

Investment & Insurance Advisor

Direct: (416) 498-6181

E-mail: kpolson@pbfinancial.com

Office Hours

Monday to Friday,

8:30 a.m. - 5:00 p.m |

| |

|

|

|

|

by Paul Bourbonniere, CFP®, CLU, CH.F.C.

As interest rates continue to disappoint, the hunt for secure income is leading many investors to consider putting their money into investment vehicles outside of their risk tolerance. For example, many companies are increasing the dividends they are paying on their common shares, making these stock investments look very attractive. Don't get us wrong - we like dividend paying stocks for the appropriate client - but they are equities, after all, and their values can fluctuate like anything else in a market downturn. We also need to keep the overall portfolio asset allocation in line with agreed upon limits. Are there any fixed income options left? In past issues we have written about a strategy we call the 'Lifetime GIC'. As interest rates continue to disappoint, the hunt for secure income is leading many investors to consider putting their money into investment vehicles outside of their risk tolerance. For example, many companies are increasing the dividends they are paying on their common shares, making these stock investments look very attractive. Don't get us wrong - we like dividend paying stocks for the appropriate client - but they are equities, after all, and their values can fluctuate like anything else in a market downturn. We also need to keep the overall portfolio asset allocation in line with agreed upon limits. Are there any fixed income options left? In past issues we have written about a strategy we call the 'Lifetime GIC'.

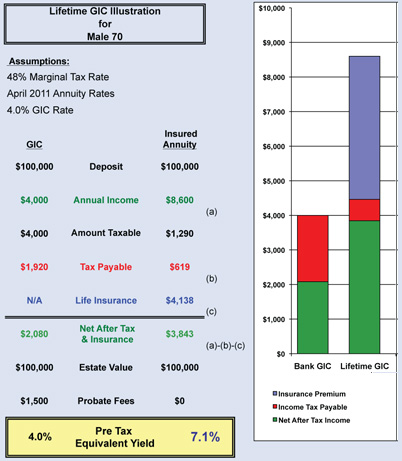

How does it work? Is it right for you? The Lifetime GIC is actually two financial products, a life annuity and a life insurance policy, combined to achieve lifetime income with full capital preservation on death. The example in the chart located on the next page shows how it works.

The annuity is a ‘Prescribed Annuity', which gives the plan certain tax advantages. Once the annuity is purchased, income continues for life, guaranteed. The life insurance (for non-smokers) premium is also fixed for life, and is discounted to reflect the increased longevity non-smokers as a group typically experience. So the Lifetime GIC works as illustrated above; a guaranteed, tax advantaged income is paid to you for life. Upon your death, the initial capital is repaid to your beneficiaries tax and probate free. Generally speaking, the older you are (65+), and the higher your tax bracket, the higher the effective interest rate you would earn on this strategy.

We are often asked about waiting until interest rates go up, to make it an even better deal. However, rates will have to increase significantly to make earning 6 or 7% equivalent immediately a bad idea. Plus, you run the risk of becoming uninsurable while you wait.

Regardless of the actual effective interest rate earned, it is worth remembering that in times of market uncertainty, receiving a guaranteed monthly income can pay huge dividends (pardon the pun) in peace of mind. Ask your Polson Bourbonniere Certified Financial Planner about the role a Lifetime GIC might play in your financial program.

In this illustration, the Insured Annuity would earn you the equivalent of 7.1% based on current annuity rates. Once issued, all Lifetime GIC values are guaranteed for life, thus protecting your investment from interest rate

and market fluctuations. |